Tech News

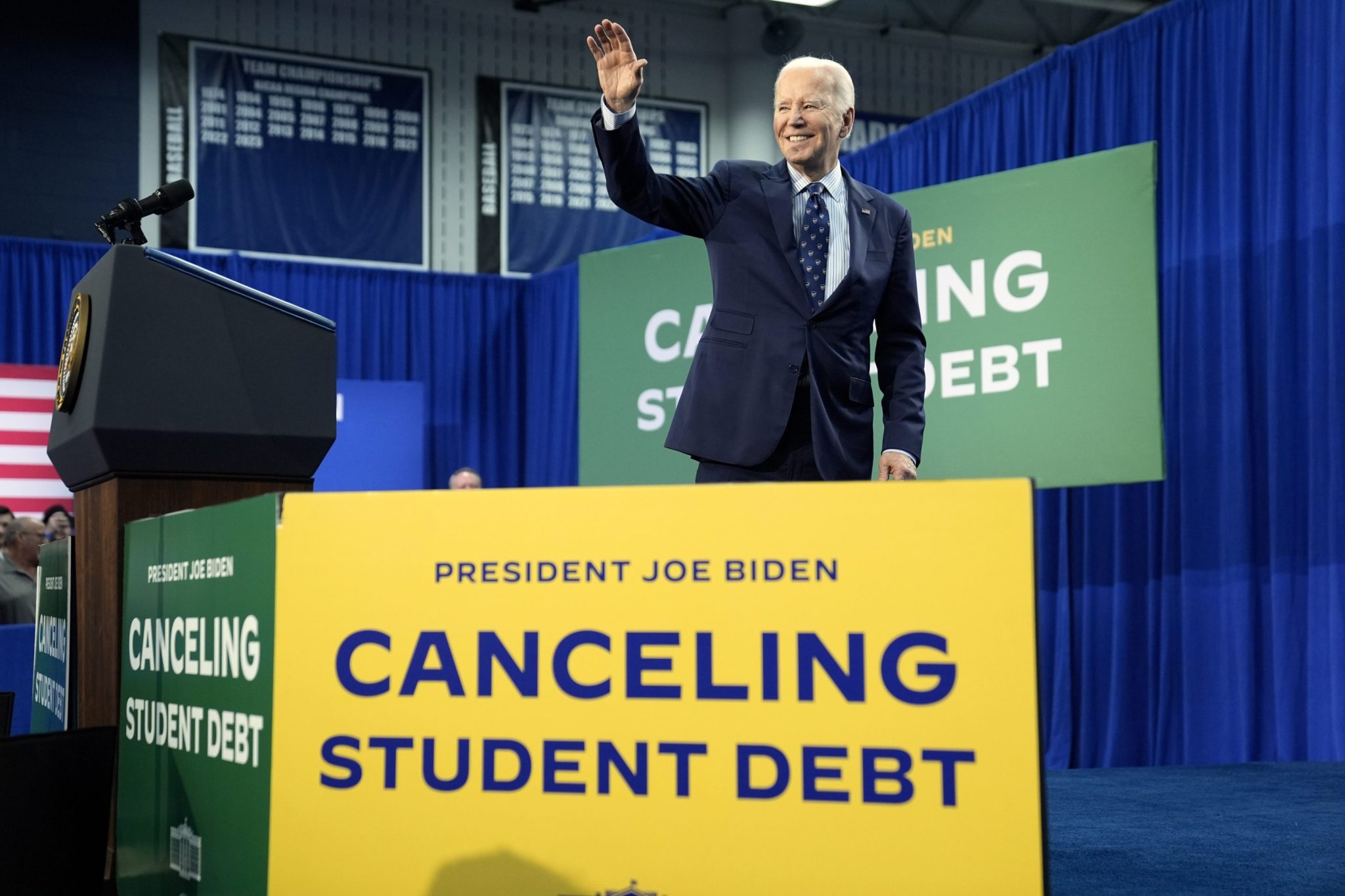

The Education Department has suspended some income-driven student loan repayment plans. Here’s what borrowers should know

The Trump administration’s recent changes to student loans are causing frustration and confusion for some borrowers.

In response to a February court ruling that blocked some Biden-era programs, the Education Department has taken down online and paper applications for income-driven repayment plans.

“This especially hurts anyone who’s lost their jobs, including federal workers,” said Natalia Abrams, founder and president of the Student Debt Crisis Center. “A few months ago, they would have been able to get on a zero-dollar income-driven repayment plan.”

The removal of application materials also has caused confusion around the recertification process for borrowers already enrolled in repayment plans, experts say. Income-driven repayment plans take a borrower’s finances and family size into account when calculating monthly payments, but borrowers must periodically demonstrate they still qualify.

Adding to the uncertainty are layoffs at the Education Department, which oversees the federal loan system. The federal website for student loans and financial aid, StudentAid.gov, suffered an hours-long outage Wednesday, but the department has said it will continue to deliver on its commitments.

“It’s been wave after wave of bad news for student borrowers,” said Aissa Canchola Bañez, policy director at the Student Borrower Protection Center.

Here’s some guidance for those with student loans.

Check with your loan servicer and know your options

All borrowers currently enrolled in income-driven repayment plans should “get a sense of when your recertification deadline is and get a sense of what options are available to you if the form is not available online to recertify your income,” Bañez said.

Recertification confirms a borrower’s financial situation. With some forms not currently available, borrowers who are unable to complete that process could be in jeopardy.

If borrowers are already on an income-driven repayment plan, they should still be allowed to remain on that repayment plan if they are able to recertify their income.

Abrams said it’s also a good idea to take screenshots of your account’s current status on the student aid website.

What other resources are available?

State-specific and state-level resources are available for student borrowers. Congress members have teams charged with helping constituents if they are having trouble with a federal agency or struggling to contact a federal student loan servicer.

Borrowers may contact their representatives in Congress and open a casework file by going onto their website or calling their office.

“Try saying something like, ‘I need your help to understand how to get into an affordable repayment option, which I’m entitled to under the law,’” Bañez said. “‘Even though this federal department has taken down these applications, I need your help.’”

Despite the thinning of the Education Department and President Donald Trump’s dismantling of the Consumer Financial Protection Bureau, loan servicers still must consider a borrower’s financial situation, Bañez said.

“You can see if you can get temporary forbearance or a deferment of payments for financial hardship,” she said.

State attorneys general also take inquiries from student borrowers.

What are affected borrowers saying?

Jessica Fugate, a government relations manager for the city of Los Angeles, said she was a less than a year from student loan forgiveness under the Biden-era Public Service Loan Forgiveness program, which forgives outstanding loans after 120 payments.

With an ongoing court challenge to her former SAVE payment plan, though, Fugate hoped to switch to an income-driven plan before Trump took office. She applied in January.

“It’s the most affordable option to repay my loans while living in Los Angeles working for the government on a government salary,” said Fugate, 42. “And it would mean my payments counted towards forgiveness.”

As of February, Fugate notified that her application was received and she had been notified of its status, but they didn’t say when she would know if she was approved.

“And when I called recently, the machine said there was a four hour wait,” she said.

With income-driven repayment plans in limbo, Fugate isn’t sure what her options are and hopes to one day have her federal loans behind her.

“I’ve been working for government for almost 10 years. After that much time, you don’t do it for the glory,” she said. “I’ve spent most of my career giving back to other people. I don’t mind serving people. I just feel this was an agreement they made with the public, and so we’re owed that. And it’s a lot of us. And we’re not just numbers.”

Debbie Breen, 56, works at an agency on healthy aging in Spokane, Washington. Breen said she has worked in the nonprofit sector for more than 10 years and that nearly all those years counted toward Public Service Loan Forgiveness.

Breen also was on the Biden-era SAVE plan, which means she was placed in forbearance when the court challenge to that plan was upheld. Like Fugate, she had planned to switch to an income-driven repayment plan to have her payments count towards forgiveness.

“I was months away from ending this nightmare,” she said. “Now I don’t think that’s going to happen. I’m kind of in panic mode because I know that if they stop income-driven repayment plans, I don’t know that I’m going to be able to afford the payments each month.”

Breen said she has two kids who also have student loans.

“They’re dealing with the same thing,” she said. “It’s scary. It’s absolutely scary.”

This story was originally featured on Fortune.com

Continue Reading

David Sacks and his investment firm Craft Ventures have divested more than $200 million in crypto holdings since President Donald Trump named Sacks as the White House’s AI and crypto czar, according to a Bitcoin, Ethereum, and Solana, according to the memo. Sacks also held stock in the online brokerage Robinhood and the crypto exchange Coinbase. And he was a limited partner in the marquee crypto venture capital funds Multicoin Capital and Blockchain Capital, along with 90 other VCs.

While Sacks has divested most of his crypto holdings, he and Craft Ventures still hold equity in a suite of companies. His shares of the crypto custody firm BitGo and the Bitcoin protocol developer Lightning Labs are worth about 2.5% and 1.1% of his total assets, respectively, according to the memo. The government, however, has agreed to waive any conflicts of interest regarding Sacks and Craft Ventures’ ongoing stakes in crypto companies.

“I sold all my cryptocurrency (including BTC, ETH, and SOL) prior to the start of the administration,” Sacks said in a post on X earlier in March.

He and his firm Craft Ventures did not immediately respond to a request for comment.

Dated March 5, the memo on Sacks’ interests in the crypto industry follows social media rumblings that the AI and crypto czar risked mixing his own business with the government’s crypto dealings. After Trump posted in early March that certain cryptocurrencies, including Solana, would be included in a national crypto reserve, critics said that Sacks was boosting his own portfolio.

And more naysayers came out against Sacks once Trump officially authorized the creation of a strategic Bitcoin reserve and a digital assets stockpile later that week. “This is a direct transfer of wealth from the U.S. treasury to David Sacks and other crypto barons,” said Ryan Grim, who runs a popular account on X and a politics newsletter.

Sacks countered that he had divested much of his cryptocurrency holdings, and crypto executives came to his defense. “He is doing tremendous work and will not be sharing in any of the economic upside to avoid even the slightest appearance of a conflict,” Cameron Winklevoss, cofounder of the crypto exchange Gemini, posted on X.

Trump named Sacks as his AI and crypto czar in December. The then incoming president said Sacks, who is a former executive at PayPal, would guide policy on the regulation of artificial intelligence and cryptocurrencies.

This story was originally featured on Fortune.com

Tech News

Dr. Oz says probiotic supplements have wide-ranging health benefits. Here’s what science says

Our bodies—and guts, specifically—depend on a balance of bacteria to “maintain healthy blood sugar and cholesterol levels,” but “you gotta feed the bacteria.” So said Dr. Mehmet Oz—heart surgeon turned daytime TV host, ardent RFK Jr. supporter, believer in disproven COVID treatment hydroxychloroquine, and now possible head of Medicaid and Medicare for the Trump administration—who began his Senate confirmation process on Friday.

To aid in that gut-balancing process, Oz has pushed the benefits of both prebiotics and probiotics, including in his role as global advisor for the iHerb brand of supplements.

Both have come under scrutiny recently, including through this week’s Washington Post opinion piece by Harvard medical school instructor and physician Trisha Pasricha, who called probiotics “a waste of money,” instead recommending a high-fiber diet.

So which doctor is right? Here’s what science tells us.

What are probiotics?

The human gastrointestinal tract is colonized by a range of microorganisms, including bacteria, archaea, viruses, fungi, and protozoa, explains the National Institutes of Health (NIH) Office of Dietary Supplements. And the activity and composition of those microorganisms (often known as the gut microbiome) can affect human health and disease.

Probiotics, according to the International Scientific Association for Probiotics and Prebiotics, are “live microorganisms that, when administered in adequate amounts,” may benefit that gut microbiome composition.

While they are naturally present in fermented foods—including the homemade turmeric sauerkraut Dr. Oz mentions in his Instagram post (above) about probiotics—they can also be added to food products, and are available as dietary supplements.

“However,” notes the NIH, “not all foods and dietary supplements labeled as probiotics on the market have proven health benefits.”

That’s where a range of varied opinions come into play.

Who says what about probiotic supplements?

As Pasricha points out, of the over 1,000 clinical trials of probiotic supplements, there have been too many different strains tested and results found to reliably say they can be universally helpful.

A 2024 review of existing evidence, published in the Advances in Nutrition journal, concluded that, on one hand, “there is sufficient evidence of efficacy and safety for clinicians and consumers to consider using specific probiotics for some indications—such as the use of probiotics to support gut function during antibiotic use or to reduce the risk of respiratory tract infections—for certain people.”

However, those researchers concluded, “we did not find a sufficiently high level of evidence to support unconditional, population-wide recommendations for other preventive endpoints we reviewed for healthy people. Although evidence for some indications is suggestive of the preventive benefits of probiotics, additional research is needed.”

When looking at the body of scientific evidence regarding effect of probiotics on seven different health issues, the NIH reports the following:

Atopic dermatitis

Numerous studies have looked at the effect of probiotics on this most common form of eczema. Overall, the evidence suggests that the use of probiotics might reduce the risk of developing atopic dermatitis, but also might provide only limited relief. The effects also depend on the strain used, the timing of administration, and the patient’s age.

Pediatric acute diarrhea

While one large review found that single- and multi-strain probiotics significantly shortened the duration of symptoms, another found it was no better than a placebo.

Antibiotic-associated diarrhea

Overall, the available evidence suggests that starting probiotic treatment with strains LGG (Lactobacillus) or Saccharomyces boulardii within 2 days of the first antibiotic dose helps reduce the risk of diarrhea in patients between 18 and 64, but not in elderly adults.

Inflammatory bowel disease

IBD is a chronic inflammatory disease that includes ulcerative colitis and Crohn’s disease, for which no cure exists. In the many reviews that have looked at the effects of probiotics, researchers reached similar conclusions—that certain probiotics might have modestly beneficial effects on ulcerative colitis but not on Crohn’s disease.

Irritable bowel syndrome

IBS is a common functional disorder of the gastrointestinal tract that’s been linked to both stress and gut microbiomes. Overall, the available evidence shows that probiotics might reduce some symptoms, but stresses that additional clinical trials are needed to confirm the specifics of strain, dose, and duration of treatment.

High cholesterol

Researchers have studied the use of probiotics to improve lipid profiles. And while, overall, research suggests that using multiple probiotic strains might reduce total and LDL (bad) cholesterol levels, more research is needed.

Obesity

Again: More research is needed. The results, the NIH concludes, “indicate that the effects of probiotics on body weight and obesity might depend on several factors, including the probiotic strain, dose, and duration as well as certain characteristics of the user, including age, sex, and baseline body weight.”

Bottom line: The jury is still out. Whether you opt to try the supplements or not (as they are generally believed to be harmless, though long-term safety studies are still needed), make sure to eat plenty of fiber as well as fermented foods. That includes yogurt, kefir, fermented cottage cheese, kimchi and other fermented vegetables (as endorsed by Oz), and kombucha tea, which were shown by Stanford University researchers to increase microbial diversity and lower inflammation.

More on supplements:

- This gastroenterologist says probiotics are ‘a waste of money.’ Here’s what you should be doing instead

- An expert says don’t waste your money on beetroot supplements—try this instead

- Coca-Cola is Olipop’s and Poppi’s latest prebiotic soda competitor. But are ‘healthy’ sodas actually good for you?

This story was originally featured on Fortune.com

Tech News

California regulator may allow State Farm to hike home insurance premiums by 22% for a million customers after devastating wildfires

California’s top insurance regulator on Friday said he would approve an emergency request by State Farm to raise premiums 22% on home insurance for about a million customers if the insurance giant could justify the hike at a public hearing.

State Farm, the state’s largest insurer with roughly 1 million home insurance policies in California, said the emergency rate would help the company rebuild its capital following the Los Angeles wildfires that destroyed more than 16,000 buildings, mostly homes. The company is trying to prevent a “dire” financial situation that executives said could push homeowners into the state’s last-resort insurance option.

California Insurance Commissioner Ricardo Lara said that other California insurers won’t be able to absorb State Farm’s customers if the insurance giant stops doing business in California, but that he wanted more data on how the company manages its finances and calculates risks. He asked the company to present its argument publicly on April 8 to a judge, who will then give a proposed decision. Lara will then make a final decision.

“State Farm claims it is committed to its California customers and aims to restore financial stability. I expect both State Farm and its parent company to meet their responsibilities and not shift the burden entirely onto their customers,” Lara said in a statement. “The facts will be revealed in an open, transparent hearing.”

Lara also called on the company to request a $500 million capital infusion from its parent company to help stabilize its finances in a private meeting this week, according to transcript of the meeting.

At the same meeting, State Farm said it would halt cancelling and not renewing policies for “at least one year” if it gets the rate increase approval. The company last year announced it discontinued coverage for 72,000 houses and apartments in California after saying it would not issue new home policies in the state in 2023.

Consumer Watchdog, a consumer advocacy group that opposed State Farm’s request, said the 22% increase could equate to an additional $600 annually for homeowners. The group previously said it would challenge the approval if Lara goes through with it.

State Farm and Consumer Watchdog didn’t immediately respond to requests for comment.

The emergency rates include a 22% rate increase for homeowners, 38% for rental owners and 15% for tenants. They will go into effect in June if Lara ultimately approves it. The decision comes as California is undergoing a yearslong effort to entice insurers to continue doing business in the state as wildfires increasingly destroy entire neighborhoods. In 2023, several major companies, including State Farm, stopped issuing residential policies due to high fire risk. Lara last year unveiled a slate of regulations all aiming at giving insurers more latitude to raise premiums in exchange for more policies in high-risk areas. Those rules kick in this year.

State Farm executives told state officials the company was already struggling before the LA fires. The company received a financial rating downgrade last year and has seen a decline of $5 billion in its surplus account over the last decade. Last year, the company asked the state for a 30% rate increase, which state officials are still considering.

The LA fires, which are now estimated to be the costliest natural disasters in the U.S. history, have made things worse, State Farm executives said. The company last month paid out roughly $1.75 billion to 9,500 claims and estimated the total loss to reach more than $7 billion. Its surplus also dropped from $1.04 billion at the end of 2024 to $400 million after the fires, according to State Farm. The company is using its surplus and reinsurance to settle the claims.

State Farm said it plans to refund the emergency rates if California later approves lower rates through the company’s request last year. The insurer last received state approval for a 20% rate increase in December 2023.

This story was originally featured on Fortune.com

-

Tech News3 months ago

Tech News3 months agoHow Costco’s formula for reaching uncertain consumers is pushing shares past $1,000 to all-time highs

-

Tech News3 months ago

Tech News3 months agoLuigi Mangione hires top lawyer—whose husband is representing Sean ‘Diddy’ Combs

-

Tech News3 months ago

Tech News3 months agoLego bricks have won over adults, growing its $10 billion toy market foothold—and there’s more to come

-

Tech News3 months ago

Quentin Tarantino thinks movies are still better than TV shows like Yellowstone

-

Tech News3 months ago

Tech News3 months agoInside the FOMC: Boston Fed President Susan Collins on changing her mind, teamwork, and the alchemy behind the base rate

-

Tech News3 months ago

Tech News3 months agoNancy Pelosi has hip replacement surgery at a US military hospital in Germany after falling at Battle of the Bulge ceremony

-

Tech News3 months ago

Tech News3 months agoTrump and members of Congress want drones shot down while more are spotted near military facilities

-

Tech News3 months ago

Tech News3 months agoHundreds of OpenAI’s current and ex-employees are about to get a huge payday by cashing out up to $10 million each in a private stock sale