Tech News

Money does buy happiness, and for one group of people, top economists say the limit does not exist

At one point in your life you’ve likely been told, “Money can’t buy you happiness.”

Two renowned economists—the late Daniel Kahneman, a winner of the Nobel Prize in economics, and University of Pennsylvania professor Matthew Killingsworth—decided to put this adage to the test.

Separately, Kahneman and Killingsworth published two different papers with conflicting results about the relationship between money and happiness. In Kahneman’s 2010 study, he and his colleague, fellow Nobel Prize winner Angus Deaton, found that happiness increases with income up until $75,000, after which it plateaus.

Killingsworth’s 2021 study, on the other hand, found that happiness increased alongside income with no limit.

In 2023, the two experts combined forces to finally answer: Is there a limit to how much money can bring you happiness?

It turns out for most people, there isn’t.

How much money you need to be happy

The acclaimed economists’ study, published in the journal PNAS, found that how happy money makes you depends on your overall emotional well-being. Drawing upon more than 450,000 responses to the Gallup-Healthways Well-Being Index, a daily survey of 1,000 U.S. residents conducted by the Gallup Organization from 2008 to 2009, researchers found that correlations between money and happiness were split into three groups based on well-being: least happy, middle-range happy, and the most happy.

They found that for the least happy group, happiness rose with income until $100,000, then plateaued. For those in the middle range of emotional well-being, happiness continued increasing linearly with income with no limit, and for the happiest group, happiness rose and then actually accelerated once they were past $100,000.

“In the simplest terms, this suggests that for most people larger incomes are associated with greater happiness,” said Matthew Killingsworth, a senior fellow at Penn’s Wharton School and lead paper author, in the press release.

“The exception is people who are financially well-off but unhappy,” he added. “For instance, if you’re rich and miserable, more money won’t help. For everyone else, more money was associated with higher happiness to somewhat varying degrees.”

One of the coauthors, professor of psychology at the University of Pennsylvania Barbara Mellers, reflected that these findings show that money and emotional well-being aren’t connected by a single relationship. Happiness is dependent on a multitude of factors—and for the most unhappy, money alone cannot change that once you reach a certain income level.

The team of researchers behind the study believe that these findings could have real-world implications beyond how people relate to money. This kind of knowledge matters to individuals navigating career choices or weighing a larger income against other priorities in life, Killingsworth said.

That being said, Killingworth emphasizes that well-being depends on much more than income.

“Money is just one of the many determinants of happiness,” he said in the press release. “Money is not the secret to happiness, but it can probably help a bit.”

Why money makes you happier

Everyone has different reasons more money would make them happier: a relief from the stressful grips of student loan debt, being able to afford a nice home, providing for kids, having money to travel, better access to quality medical care, and creating a cushion for retirement.

But there are other factors at play when it comes to income and happiness.

Forbes reported that the late happiness researcher Ed Diener—nicknamed Dr. Happy—wrote in his book Happiness, “Financial resources can serve as a buffer against life’s negative events,” meaning that more money allows you to avoid the life stressors and worries that can come with being less fortunate.

Humans also often fear scarcity, according to University of Texas professor Raj Raghunathan. He notes in his book If You’re So Smart, Why Aren’t You Happy?, that feeling like we have enough is crucial to happiness: “When we are feeling abundant, life seems like a cozy mess: perfect despite its imperfections.” With that comes a sense of security, feeling like we have access to all the resources we could need.

More money also leads to a greater sense of freedom, according to sociologist Rachel Sherman and author of the book Uneasy Street: The Anxieties of Affluence. When she asked wealthy New Yorkers about the benefits of being wealthy, many responded that it provided freedom, a sense of control over their lives, and a feeling of autonomy.

Lastly, your happiness also depends on how you use your money. A 2017 study found that using money to buy time—specifically, buying time-saving services like help with common household chores such as cleaning, shopping, and cooking—increased happiness. Other research indicates that spending money on others and prioritizing experiences over material possessions both promote greater happiness.

For more on happiness:

- These are the 10 happiest cities in America, according to new research

- Researchers have followed over 700 people since 1938 to find the keys to happiness. Here’s what they discovered

- What time of day you feel your best and worst, according to research

- Hawaii is the happiest state in America. Here’s how the rest of the country ranks

This story was originally featured on Fortune.com

Continue Reading

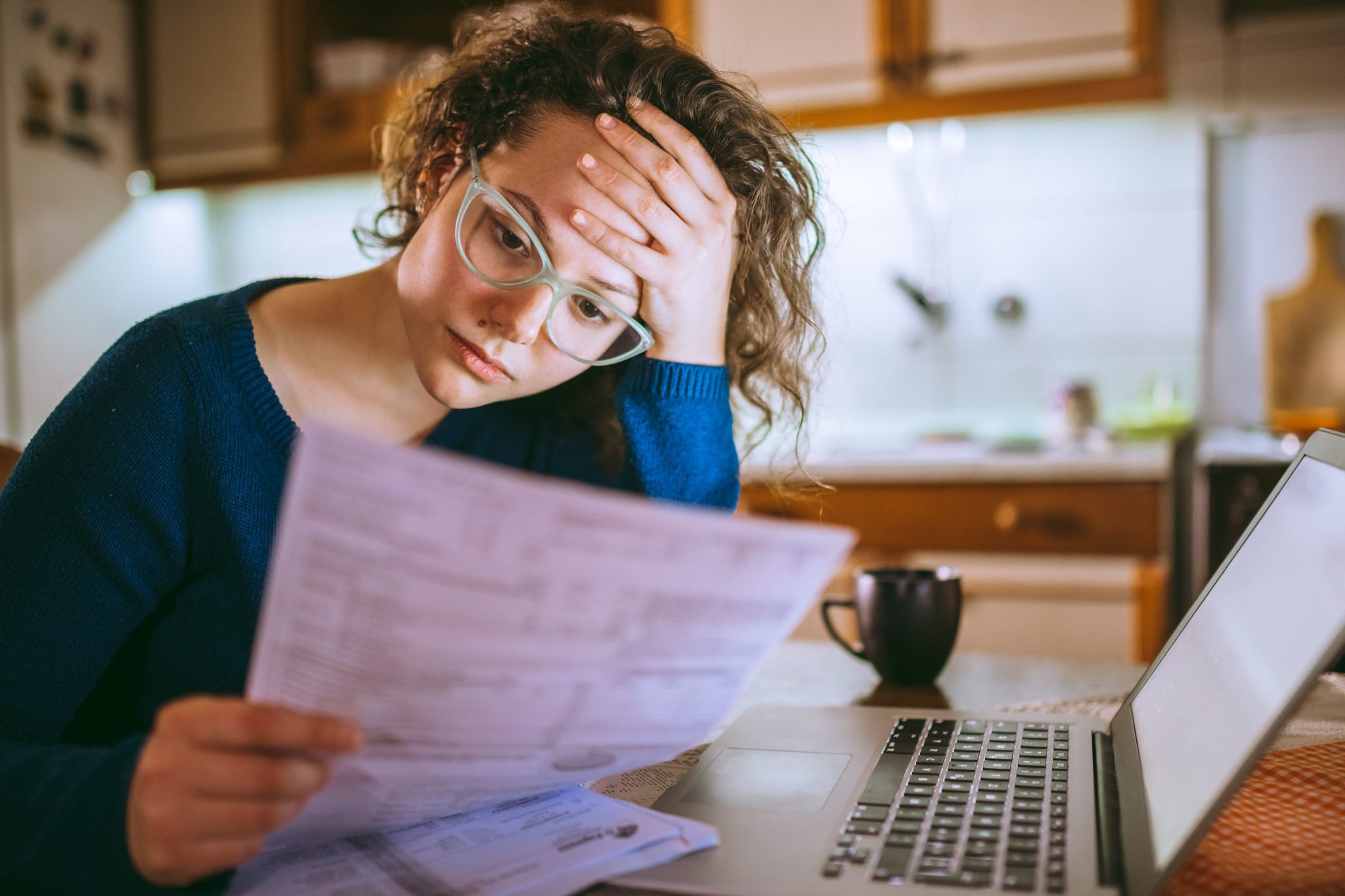

A growing share of US consumers say they’re not seeking loans because they expect to be refused amid tight credit conditions, according to data from the Federal Reserve Bank of New York.

The share of discouraged borrowers, defined as respondents who said they needed credit but didn’t apply because they didn’t expect to get approved, climbed to 8.5% in the New York Fed’s latest Survey of Consumer Expectations. That’s the highest level since the study began in 2013.

The perceived likelihood of being rejected increased across different forms of credit, from cards to secured loans to buy homes and cars. Roughly one-third of auto loan applicants expected to get turned down, the highest share since the start of the series, while nearly half of all respondents in the February survey said it’ll be harder to get credit in a year’s time.

The data adds to a picture of increasingly fragile household finances for many Americans, as a cooling job market slows wage gains while high borrowing costs are making bills harder to pay. Delinquency rates remain low by pre-pandemic standards but they’ve been edging higher in most categories, and lenders are turning cautious.

More than four in 10 US homeowners who sought to refinance their mortgages had their applications rejected, according to the February survey, quadruple the share in October 2023.

With mortgage lending rates still much higher than a couple of years ago, many people seeking a refi are likely trying to tap equity accumulated during the recent housing boom in order to meet other debt costs or expenses, rather than to reduce their monthly payments. Inability to do so could put some under pressure to sell their homes.

Meanwhile, the share of consumers in the New York Fed survey who said they could come up with $2,000 in the event of an unexpected need declined to 63%, a new series low.

This story was originally featured on Fortune.com

The head of Canadian jet manufacturer Bombardier Inc. raised concerns about Canada’s decision to review a contract to buy dozens of F-35 fighter jets from Lockheed Martin Corp., the country’s latest response to the trade war with the US.

“Canceling the F-35s might be a good idea, but we need to think about it,” Bombardier Chief Executive Officer Eric Martel told a business audience in Montreal. “We have contracts with the Pentagon. Will there be reciprocity there?”

Bombardier has invested in recent years in its defense unit, which converts jets into military aircraft. It has two contracts with the US government, one for communication aircraft and another for surveillance planes.

New Canadian Prime Minister Mark Carney ordered a review of the F-35 purchase agreement, a C$19 billion ($13.3 billion) deal for 88 jets that was finalized in 2023. The deal hasn’t been scrapped, but the government needs to “make sure that the contract in its current form is in the best interests of Canadians and the Canadian Armed Forces,” a defense ministry spokesperson said.

Earlier this month, President Donald Trump put 25% tariffs on imports on Canadian goods that don’t fall under the US–Mexico–Canada Agreement, and added 25% import taxes to aluminum and steel products. He has repeatedly said he believes Canada should be the 51st US state — a recent poll showed that 90% of Canadians disagree — and members of his administration have taken the Canadian government to task for its low level of military spending.

“Trump isn’t wrong on everything,” Martel said. “We’ve been hiding behind our big brother for a while, and we’re completely dependent on him militarily.”

In 2023, Canada finalized a deal to order as many as 16 military surveillance aircraft from Boeing Co. as part of an investment worth more than $7 billion, rejecting a competing Bombardier proposal.

The jet maker’s shares have dropped 18% since Trump was elected on Nov. 5, but are still up about 50% over the past year.

In February, Bombardier set aside its financial outlook for the year because of risk and uncertainty about tariffs. “Not providing guidance is the most responsible thing for us to do,” Martel said at the time. About 60% of Bombardier’s business comes from the US, and its planes are currently built and shipped under the rules of the US-Mexico-Canada Agreement.

Bombardier has a complicated supply chain that includes manufacturing in US and Mexico with more than 2,800 US-based suppliers across 47 states. US-made parts and systems make up a significant proportion of the cost of its aircraft.

The Global 7500, the firm’s flagship jet, has wings made in Texas, avionics from Iowa and motors made in Indiana. More than half of its building costs are tied to US manufacturing, but the assembly and finishing are done in Canada, which makes the jet subject to tariffs.

Two-thirds of Canada’s aerospace industry exports depend on the US market, Martel said.

This story was originally featured on Fortune.com

Tech News

Gavin Newsom is welcoming prominent conservatives on his new podcast, but critics say it’s risky to align himself ‘in a slightly unpredictable middle’

LOS ANGELES (AP) — As a wounded Democratic Party struggles to regroup, California Gov. Gavin Newsom is holding mostly chummy conversations with prominent conservatives on a new podcast he’s touting as a way for the party to grapple with the MAGA movement’s popularity.

In doing so, he appears intent on showing he is more than a progressive warrior. But he has stunned some members of his own party by agreeing with his guests on issues such as restricting transgender women and girls in sports. Newsom called dismantling police departments “lunacy” and remained silent when Steve Bannon, an architect of President Donald Trump’s 2016 campaign, falsely said Trump won the 2020 presidential election.

The programs provide a fresh lens on a liberal governor and potential 2028 presidential candidate who not long ago was enlisted as a chief surrogate for President Joe Biden’s campaign. Ahead of the 2022 midterms, he chastised national Democrats for being too passive in defending abortion rights and same-sex marriage, an issue he championed two decades ago as mayor of San Francisco.

Newsom said his choice of podcast guests reflects his interest in knowing more about how Republicans organized in the last election, when Trump swept every battleground state and Republicans locked up majorities in the House and Senate.

“I think we all agreed after the last election that it’s important for Democrats to explore new and unique ways of talking to people,” he added in an email to supporters.

Newsom’s party criticizes his guests

After spotlighting Bannon, conservative radio personality Michael Savage and Turning Point USA founder Charlie Kirk, Newsom will quickly diversify his lineup: His next guest is Minnesota Gov. Tim Walz, last year’s Democratic vice presidential nominee. But some Democrats say the governor, who is widely viewed as having presidential ambitions, is selling out Democratic values in favor of his own political aspirations.

Aimee Allison, the founder and president of She the People, a national organizing hub for electing women of color, said Newsom is betraying California and “showing his weakness and naked ambition.” Allison was among Democrats who helped Newsom defeat a 2021 recall attempt.

“We need a governor that will defend California’s values, support vulnerable children, LGBTQ+ people, Black people, women, and everyone else who’s in the line (of) fire of the Trump administration. Instead he is making the worst moves possible in a time of rising fascism. He’s trying to remake himself to be acceptable to MAGA,” Allison wrote in an email, referring to supporters of Trump’s “Make America Great Again” movement.

California Assembly member Chris Ward and state Sen. Carolina Menjivar, who lead the state’s LGBTQ+ legislative caucus, said they were “profoundly sickened” by Newsom’s statement on transgender athletes. And Kentucky Gov. Andy Beshear, another potential 2028 candidate, said of Bannon, “I don’t think we should give him oxygen on any platform — ever, anywhere.”

Finding a new audience

Podcasts have become an increasingly important venue in politics, and as Newsom considers a national campaign he has been praised by some for venturing into unfamiliar territory.

Democratic consultant Bill Burton, who was national press secretary for former President Barack Obama’s 2008 campaign, credited Newsom with trying to reach voters who might not engage with traditional media.

“I think there are going to be a lot of people this alienates in the short term,” Burton said. But, he added, Democrats “have to take a lot of big swings.”

The governor — who called Trump a threat to American democracy throughout last year’s campaign — has been trying to navigate a tenuous relationship with the White House as the state recovers from the devastating Los Angeles wildfires in January. He’s requested $40 billion in federal aid.

Newsom, while progressive, has never been locked into one ideological position: He’s broken at times with more liberal factions in the Legislature. His shift this time may be to head off the kind of criticism Republicans have aimed at former Vice President Kamala Harris, also of California, or edge toward positions more closely in line with public opinion. According to AP VoteCast, 55% of voters nationwide in the 2024 election said support for transgender rights in government and society has gone too far.

During the podcast episodes released so far, Newsom has been mostly affable and agreeable, though he’s challenged his guests at times. This is not the tart-tongued Newsom who appeared in a 2023 televised debate with Republican Florida Gov. Ron DeSantis, whom he described as weak and pathetic, or who called the state legislature into special session last year to attempt to safeguard the state’s progressive policies under a Trump administration.

In an age of rigid partisanship, talking with the other side is “so rarely a part of public discourse it seems like either bravery or lunacy,” said Thad Kousser, a political science professor at the University of California, San Diego. “While there are clear risks, he is trying to align his national reputation … in a slightly unpredictable middle.”

This story was originally featured on Fortune.com

-

Tech News3 months ago

Tech News3 months agoHow Costco’s formula for reaching uncertain consumers is pushing shares past $1,000 to all-time highs

-

Tech News3 months ago

Tech News3 months agoLuigi Mangione hires top lawyer—whose husband is representing Sean ‘Diddy’ Combs

-

Tech News3 months ago

Tech News3 months agoLego bricks have won over adults, growing its $10 billion toy market foothold—and there’s more to come

-

Tech News3 months ago

Quentin Tarantino thinks movies are still better than TV shows like Yellowstone

-

Tech News3 months ago

Tech News3 months agoInside the FOMC: Boston Fed President Susan Collins on changing her mind, teamwork, and the alchemy behind the base rate

-

Tech News3 months ago

Tech News3 months agoNancy Pelosi has hip replacement surgery at a US military hospital in Germany after falling at Battle of the Bulge ceremony

-

Tech News3 months ago

Tech News3 months agoTrump and members of Congress want drones shot down while more are spotted near military facilities

-

Tech News3 months ago

Tech News3 months agoHundreds of OpenAI’s current and ex-employees are about to get a huge payday by cashing out up to $10 million each in a private stock sale